The ability of the DJI to retrace all the way to a nominal new high indicates that we are indeed in a 5th up to the mid-April I1 high.

QE2 stated the intent to purchase $600Billion of treasury securities. There was no warranty, written or implied, that there would be a similar increase in the Fed balance sheet. Since 8/11/2008 the balance sheet has increased $300Billion.

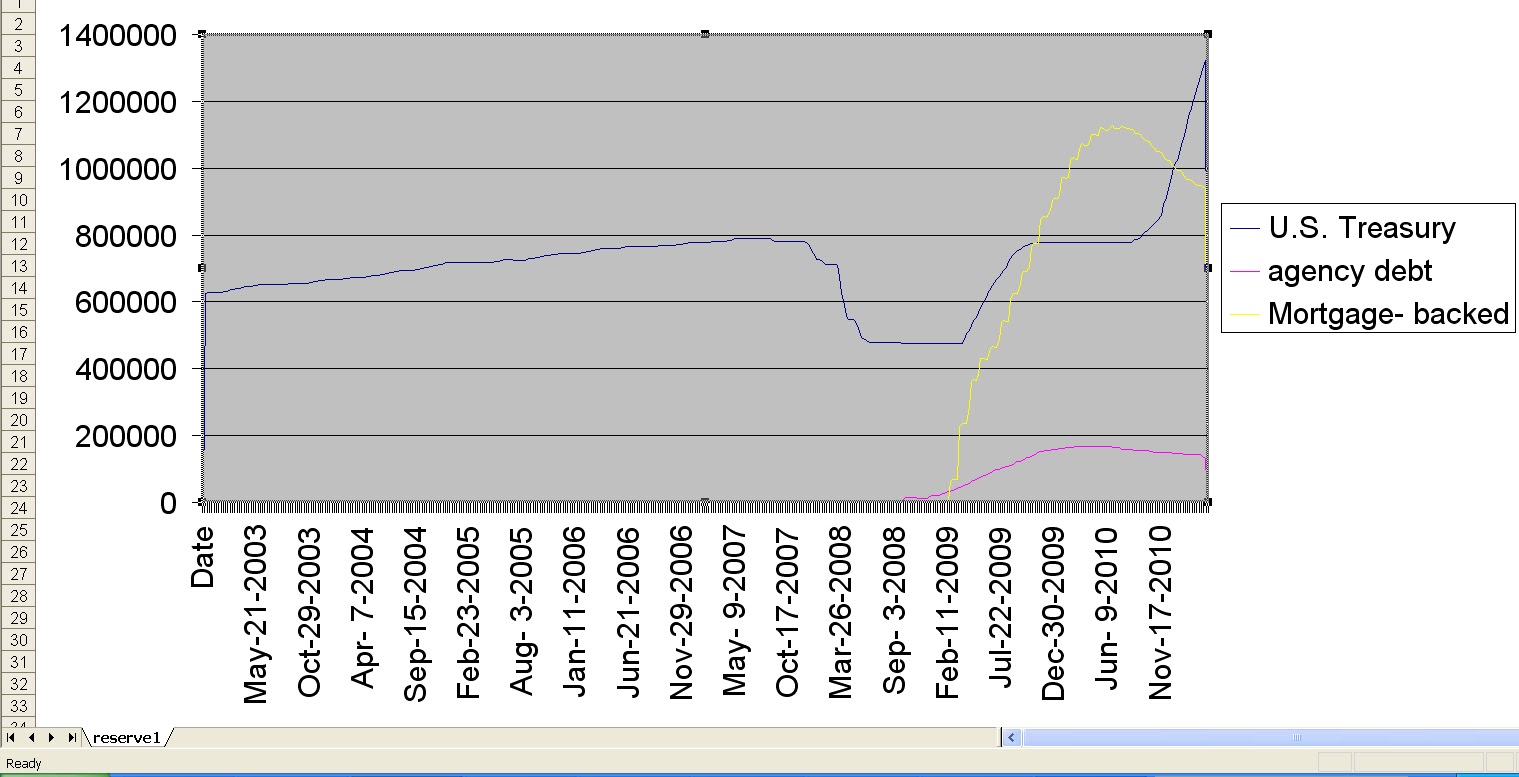

The tripling of the Fed balance sheet since 9/2008 has caused an explosion in worldwide commodity prices by providing cheap and easy money to hedge funds to guide prices ever upward. Ben quotes U.S. stated inflation as tame, by quoting CPI ex-food and energy. The cycle goes thus, first the reserve currency expands it's base and, since foreign contracts are on the whole denominated in dollars, there arises foreign commodity inflation in local currencies along with their stock markets, then foreign CPI which is much more commodity-sensitive than the U.S., and the circle arrives back in the U.S. with pre-cursors to domestic inflation in industrial commodities. Only after this has gone full circle will inflation register in PPI followed by CPI because companies producing physical products in the U.S. will be forced to raise prices, first wholesale, then retail.

The UN food index has been steadily hitting new record highs, as evidenced by the riots throughout the mideast and will bleed into the Phillipines and other third-world Asian countries with high unemployment and a youthful demographic.

We have already experienced a burst of industrial commodity prices as well as grains and meats priced in dollars. The following is 24-month change in CRB industrial commodity index which does not include any foods:

Profit margins are going to be squeezed, then finally wholesale and retail prices will go up. The stock market cares deeply about margins. The last spike of this magnitude was 1973-74, the worst inflation-adjusted stock market since 1930-32. This places the Fed in a box because if they wait too long and continue to key policy on the stock market they will commit the same mistakes as the Burns and Miller Fed chairmanships, leading to hyper-inflation fears and a decimated bond market.

The next stage in the inflation pipeline, after the Fed exports inflation around the world and it arrives back in industrial commodities, is the PPI.

Here is the 24-week rate-of-change of the monetary base:

Steve,

ReplyDeleteI know you are holding EUO. Do you think there will be much of a dollar rally early this week?

Thanks,

Dan

If the June Euro stays below 1.423 I expect a decline into Wednesday. If the dollar breaks 77 on the upside then I'll stay in EUO. I bought EUO on the Euro testing old highs.

ReplyDelete